What is Materiality and why it matters in business

Materiality is crucial for ESG and sustainability reporting because it allows companies to focus on the most important aspects of their sustainability efforts.

A company can choose to report on all aspects of its ESG and sustainability program, but this would be time-consuming and would probably not be very useful for investors and other stakeholders who want to know about how a company is handling its impacts on the environment and society, and how it is impacted by broader ESG issues.

What is Materiality?

Materiality refers to identifying the issues that matter most to a company’s business and stakeholders and determining how important they are.

By focusing on material issues, companies can make sure they are reporting on the most important issues and communicating what's useful and informative.

Definitions of materiality often differ across different ESG frameworks.

Principles and concepts

Objectives behind the concept of impact

Generally, there are three approaches to materiality:

- financial materiality

- double materiality

- dynamic materiality

Different regions and organisations may favor one approach over the others, although preferences will likely shift and evolve as ESG reporting advances (see table at the end of this section).

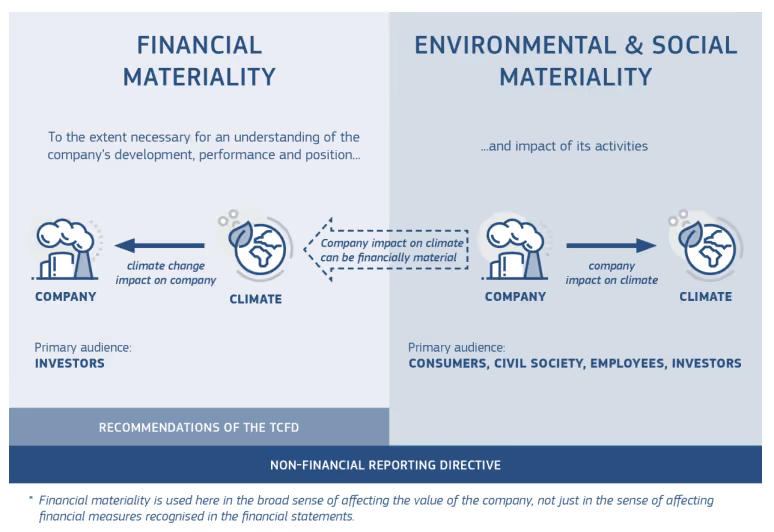

Financial Materiality

- Financial Materiality seeks to identify information that is likely to impact a company’s financial performance.

Financial materiality focuses on investors; it is shareholder-oriented and pays key attention to external factors that are likely to affect the financial performance of an organisation

For instance, a financial materiality approach might consider the issue of corruption material if fines were levied on the company.

The financial materiality approach is common among US and UK regulations and organisations.

Double Materiality

- Double Materiality is a combination of financial materiality and impact-based materiality.

Impact-based materiality determines materiality by assessing whether a company’s activities might have a significant impact on the economy, environment and people.

For instance, an impact-based materiality approach might consider climate change a material issue for a company that is carbon-intensive, because that company is negatively impacting the environment.

This emphasis on external impacts and a broad set of stakeholders differs from the definition of materiality typically used to guide financial reporting, which is focused on financial impacts of interest to investors.

{{encartSpecial}}

Given that double materiality incorporates both the financial perspective and the impact-based perspective, the double materiality approach encourages corporations to consider the impact of ESG concerns on the company’s value creation and on stakeholders (governance, environment and people).

The concept of double materiality was first proposed by the European Commission in 2019, and is more commonly adopted in European Union countries.

The Non-Financial Reporting Directive (NFRD) and the European Financial Reporting Group (EFRAG) both acknowledge double materiality as key for ESG and sustainability reporting.

Dynamic Materiality

- Dynamic Materiality proposes that issues that were not previously considered may become material over time, and that there are certain triggers for this process.

Dynamic materiality is the most recent addition to materiality assessments, and was first introduced in early 2020 by the World Economic Forum (WEF).

Dynamic materiality takes the perspective that materiality is a process that unfolds over time. According to this approach, what is financially immaterial to an organisation today can become material tomorrow. It emphasises on the need for organisations to be forward looking and proactive.

The theory behind dynamic materiality is that businesses in the early stages of growth may negatively impact society because they lack the resources or experience to identify and fully address some issues as material.

However, changing norms such as stakeholder activism, regulations, and/or corporate innovation may eventually motivate the company to adjust their materiality assessment and take action on the issues that they had previously overlooked.

Thus, from the dynamic materiality perspective, materiality evaluations are not static. Rather, materiality assessments present an opportunity for strategic foresight and consideration of external driving forces that may impact the company’s way forward.

Implications for companies

Materiality assessments are the process by which companies identify and understand the issues that are most important to their practice, given their unique business model and operations.

Materiality analyses are beneficial to corporations for it provides insights into future trends, contributes to the company’s overall risk assessment, and monitors the topics that are important to stakeholders. Materiality assessments also contribute to transparency and accountability in a company’s processes, and therefore, indirectly contributes to stakeholder satisfaction.

Furthermore, not completing a materiality assessment presents financial, reputational, and legal risks. Forgoing a materiality assessment could mean missing key issues, failing to address stakeholders’ concerns, and/or failing to build resilience for future events.

Thus, there is currently a growing demand for materiality analysis, as investors and even governments increasingly see this process as part of a necessary due diligence effort.

A materiality analysis is usually illustrated by a materiality matrix, as shown in the example below.

Practical approaches and implementation of materiality assessments

The steps for a materiality assessment may vary depending on the process that the company in question wants to take.

However, the steps below provide an idea of what the process generally looks like.

Identify stakeholders

Gather insights from both:

- Internal stakeholders (eg. Board members, employees, executive leadership, managers, etc).

- External stakeholders (eg. Customers, investors, peer companies, local communities, etc.)

Conduct initial stakeholder outreach

Develop a communication strategy and utilise contextually appropriate outreach channels, either qualitative (interviews with stakeholders) or quantitative (surveys and other hard data collection) – both are necessary to gain a holistic understanding of stakeholder values and expectations.

Design and launch materiality survey

- Identify topics that the company will use to assess/determine priority issues. Material topics are often categorised according to ESG parameters (eg. Environmental, Social, Governance issues), sometimes with the addition of economic indicators.

- Launch and disseminate the survey to relevant audiences

Articulate insights from the survey

Rate the results based upon the predefined scoring methodology. Review both quantitative and qualitative aspects.

The key end result should be a formal matrix graph that plots how each issue ranks in significance relative to stakeholder expectations.

Such graphs, called materiality matrices, are useful in visualising and mapping out the universe of issues that the company is considering.

Gain necessary approval and support

- Ensure that the materiality analysis results in a clear roadmap (i.e. targets and policies on the most material issues) that is aligned with overall corporate strategy/mission

- Make sure relevant internal and external stakeholders are involved in this roadmap

- Put proper oversight processes into place for accountability purposes

Disseminate and communicate the results and/or take action

Share the results from the materiality assessment. This is usually done through a formal CSR report, and is later disseminated through channels such as the official company website or other media.

To conclude...

Materiality assessments are crucial aids for companies to prioritise what needs to be addressed first, so they can focus on the most important aspects of their sustainability efforts, instead of getting distracted.

So, what are you waiting for?

If you want to succeed in your sustainable journey… Save time and begin the process today with Apiday!

We’ll support you through your materiality assessment and identify where your energy should be dedicated, with a step-by-step roadmap.

Don't miss out on this opportunity. Try our tool today and unlock your organisation's true potential!

Uncover Hidden Opportunities for Growth with our Materiality Assessment Feature

Enhance your sustainability and competitiveness with our tool that identifies and prioritises the most important sustainability issues and opportunities. Collect data, analyse, and assess with ease, optimising resource allocation and contributing to a more sustainable future. Try it today!

Frequently Asked Question

The concept of materiality refers to the notion of companies identifying and prioritising topics that are of greatest importance to them and their stakeholders.

Materiality is important for ESG reporting reporting because companies have limited resources, and therefore must be able to define what are the key issues they should focus on.

When conducting a materiality assessment, steps may vary but usually include: identifying stakeholders, conducting initial stakeholder outreach, designing and launching the materiality survey, analysing insights from the survey and illustrating findings in a materiality matrix.

Related articles

What is the Sustainability Accounting Standards Board (SASB) and how does it work?

The SASB Standards cover a range of environmental, social, and governance (ESG) topics, and are designed to be compatible with existing financial reporting frameworks.

What is the ESG reporting standards landscape?

Explore the ESG reporting standard landscape and find the right fit for your organisation.

What is the ESG reporting regulations landscape?

Explore the ESG reporting standard landscape and find the right fit for your organisation.