EU Taxonomy compliance: how to prepare & key dates

To reach the objectives of the European Green Deal, including the 2050 climate-neutrality target, it is crucial that investments are directed towards sustainable projects and activities. To achieve this, a clear definition must be established to properly define what constitutes as “sustainable” to avoid greenwashing. Therefore, the action plan on financing sustainable growth called for the development of a unified classification system for sustainable economic activities, known as the EU Taxonomy.

Published in the EU's Official Journal on June 22, 2020, the EU Taxonomy Regulation entered into force on July 12, 2020. This article will explore what the Taxonomy is and how it works. We will also highlight In how your business can effectively align with the Taxonomy, ensuring that each step you take towards sustainability is strategic and delivers significant impact.

What is the EU Taxonomy?

The EU Taxonomy is one of the key aspect of EU’s sustainable finance framework and is a classification tool which provides clarity for companies, capital markets, and policy makers on which economic activities are sustainable. By defining what can be considered sustainable and creating a frame of reference for investors and companies, it plays an important role in protecting against greenwashing practices and help the EU scale up sustainable investments.

How does the EU Taxonomy work?

To help direct investments to green investment, it has created a framework and principles for assessing economic activities against six environmental objectives. Each objective has a set of “technical screening criteria” (TSC) detailing the specific thresholds and requirements for each activity to be considered as signficiantly contributing to a sustainability objective.

The six environmental objectives are:

- Climate change mitigation

- Climate change adaptation,

- Sustainable use and protection of water and marine resources,

- Transition to a circular economy,

- Pollution prevention and control, and

- Protection and restoration of biodiversity and ecosystems.

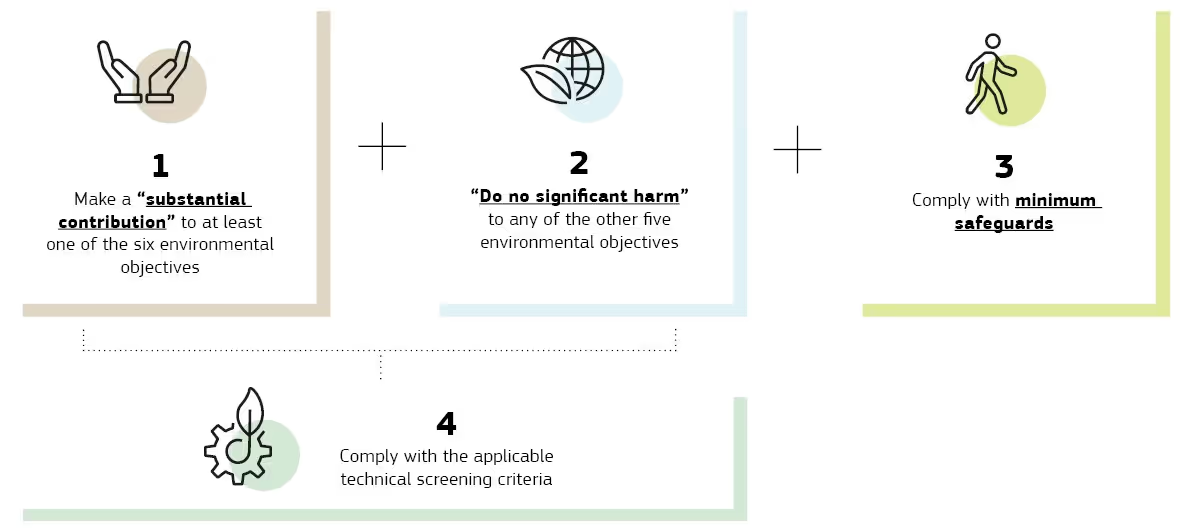

For an activity to be considered “sustainable,” it must:

- Contribute to at least one of six environmental objectives*,

- Do no significant harm (DNSH) any of the other objectives*,

- Comply with Minimum Social Safeguards (basic social criteria such as respecting basic human rights and labour standards aligned with the OECD Guidelines for Multinational Enterprises and the UN Guiding Principles on Business and Human Rights).

*To qualify for conditions 1 and 2, the activity must comply with the applicable TSC

In addition to the six economic activities listed above, the Taxonomy recognises two other subsets of activities.

Enabling activities

The Taxonomy recognises that some activities can make a substantial contribution to the EU’s climate and environmental goals by “directly enabling” other activities to improve their performance and make a substantial contribution to one or more of the objectives. This is provided that the enabling activity:

- Does not lead to a lock-in of assets that undermine the long-term environmental goals, considering the economic lifetime of those assets, and

- Has a substantial positive environmental impact, based on life-cycle consideration

- Transitional activities: for which no low-carbon alternatives are yet available, but which are extremely important to support the urgent transition to a climate-neutral economy.

Transitional activities can be included as Taxonomy-aligned activities provided that they have:

- Greenhouse gas emission levels that correspond to the best performance in the sector or industry

- Do not hamper the development and deployment of low-carbon alternatives,

- And do not lead to a lock-in of carbon-intensive assets, considering the economic lifetime of those assets

The EU Taxonomy covers technical screening criteria for many industries spanning from forestry to waste management to education to tourism. To find out more about the specific industries and activities currently covered, click here.

Who is affected?

Member States and the EU: When they claim public measures, standards, or labels for financial products or corporate bonds are environmentally sustainable.

- Financial Market Participants: they must disclose how and to what extent their investments support economic activities that meet the criteria for environmental sustainability under the Taxonomy Regulation. If investments do not align with taxonomy-compliant activities, a statement must be made indicating this.some text

The EU Taxonomy interacts with the EU’s Sustainable Finance Disclosure Regulation (SFDR) as all Article 8 and 9 products will have to disclose the proportion of their underlying investments that is aligned with the Taxonomy.

- Financial and Non-Financial Companies: those under the Non-Financial Reporting Directive (now Corporate Sustainability Reporting Directive (CSRD)) must now disclose how and to what extent their activities are associated with environmentally sustainable economic activities. This applies to large public-interest companies with over 500 employees, covering around 6,000 large companies and groups across the EU.

The EU Taxonomy can also be used voluntarily by market actors not covered by the NFRD. For companies who decide to declare voluntarily, this can help them gain market access to sustainable. For example, SMEs not required to publish a non-financial statement might share their Taxonomy Regulation alignment on their websites to attract investment.

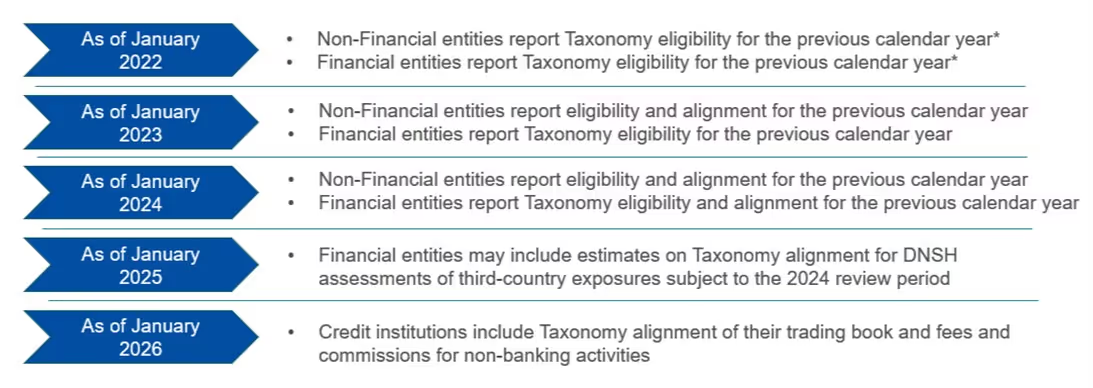

Timeline

The reporting obligations and timelines (4) for undertakings are set out in the Disclosures Delegated Act supplementing Article 8 of the Taxonomy Regulation.

What’s next?

Today's Taxonomy does not yet have an exhaustive list of environmentally sustainable economic activities, but instead defines a general framework for what economic activities qualify as “environmentally sustainable.” It is a living document which will continue to evolve and develop over time.

It is important to note that just because an activity is not included in the Taxonomy at the moment does not indicate it is unsustainable. It just means that criteria have not yet been developed for these activities are therefore are not yet eligible under the EU Taxonomy.

With the adoption of the Corporate Sustainability Reporting Directive (CSRD), businesses will be required to publish data on environmental performance that is not Taxonomy-aligned. Therefore, industries or activities not presently covered by the EU Taxonomy due to their limited contribution to the six environmental objectives will still have the opportunity to report their environmental performance to financial market participants through the CSRD.

{{encartSpecial}}

A comprehensive approach to preparing for the EU Taxonomy

Assess eligibility and regulatory compliance

Begin by understanding your company's profile, including the number of workers, sector, and turnover. Determine whether compliance with EU regulations such as the EU Taxonomy, SFDR, and CSRD is necessary.

Identify eligible business activities

Map your economic activities to the EU Taxonomy to ascertain which are eligible for alignment. Understand the significant contributions and potential Do No Significant Harm (DNSH) implications.

Evaluate social safeguards compliance

Consider compliance with minimum social safeguards, ensuring adherence to international human and labour rights standards outlined in OECD guidelines, UN Guiding Principles on Business and Human Rights, and relevant labour rights conventions.

Compile mandatory disclosures report

Prepare a comprehensive report on mandatory disclosures, detailing the extent of alignment with the EU Taxonomy and other relevant regulatory requirements.

Seek external assurance

Pursue external assurance for your Taxonomy-related disclosures, following industry best practices and standards to enhance credibility and transparency.

It is also possible that additional internal controls will need to be created in order to report trustworthy Taxonomy-aligned disclosures - and that even more strategic considerations about the future-proofness of one's business model will emerge as a result of this.

The key importance of data collection

Moving forward, the formulation of an effective and unified strategy is contingent upon the establishment of a proper data structure. Data collection should be conducted per the Taxonomy to periodically ascertain the degree to which the business goals and objectives correspond with those of the EU Taxonomy.

After analysing and understanding the gathered data, enterprises should determine whether their activities fall under the EU Taxonomy, and devise a tailored strategy according to their status:

Apiday’s hassle-free EU Taxonomy compliance module

Navigating the complexities of the EU Taxonomy can be challenging, but Apiday’s comprehensive solution simplifies this critical process for investors and companies alike. Here’s how Apiday stands out:

Eligibility screening and alignment

Apiday's platform includes advanced screening tools that help you quickly determine whether your activities are eligible under the EU Taxonomy and ensure these activities align with the requirements of the EU regulations.

Guided workflows and simple assessments

Apiday offers detailed, step-by-step workflows that guide you through each stage of the compliance process. The platform asks straightforward, easy-to-understand questions that help you assess your activities’ substantial contribution, compliance with the “Do No Significant Harm” criteria, and adherence to minimum safeguards.

End-to-end solution

Our module is not just a tool—it’s a full-service solution that supports companies and investors through the entire process of EU Taxonomy compliance, from initial assessment to final reporting. Apiday's modules provide an all-encompassing, easy-to-use platform that ensures you are fully compliant with all major EU regulations, thereby enhancing your operational efficiency and sustainability reporting.

Take advantage of Apiday to stay ahead of the industry!

Streamline your compliance journey with Apiday!

Our EU Taxonomy module takes the pain and guesswork away - from eligibility screening and aligning to outputting the required RTS reporting. Whether you are an investor or a company, Apiday’s EU Taxonomy feature delivers an end-to-end solution for you. Try it today!

Frequently Asked Question

The EU Taxonomy is a classification system that establishes a list of environmentally sustainable economic activities, aiming to guide investments towards climate-friendly projects and prevent greenwashing. It outlines six environmental objectives and requires companies to report on their alignment with these criteria.

The EU Taxonomy has six environmental objectives: climate change mitigation, climate change adaptation, sustainable use and protection of water and marine resources, transition to a circular economy, pollution prevention and control, and protection and restoration of biodiversity and ecosystems.

The EU Taxonomy itself is largely optional, but entities that fall under EU regulations such as the Corporate Sustainability Reporting Directive (CSRD) and the Sustainable Finance Disclosure Regulation (SFDR) are required to report on how their operations align with the Taxonomy's criteria.

Sources

Related articles

What is the Sustainability Accounting Standards Board (SASB) and how does it work?

The SASB Standards cover a range of environmental, social, and governance (ESG) topics, and are designed to be compatible with existing financial reporting frameworks.

What is CSR (Corporate social responsibility) and how to adopt it?

CSR is an abbreviation for Corporate Social Responsibility. CSR strategies have become common in today’s corporate world as more and more companies realise that their business performance and its societal impacts are intricately connected.

What is the ESG reporting standards landscape?

Explore the ESG reporting standard landscape and find the right fit for your organisation.