What is the Task Force on Climate-Related Financial Disclosures (TCFD) and why does it matter?

The Task Force on Climate-Related Financial Disclosures (TCFD) recommendations provide guidance to all market players regarding the disclosure of information about the financial impacts of climate change.

By helping stakeholders to better understand how a company's assets are concentrated in carbon-based products and services, as well as how exposed individual companies and the financial system more broadly are to climate-related risk, the TCFD is intended to encourage more informed investment and lending decisions.

What is TCFD?

The Financial Stability Board (FSB) established the Task Force on Climate-Related Financial Disclosures (TCFD) in 2015 to provide uniform climate-related financial risk disclosures for corporations, banks, and investors when communicating with stakeholders.

In 2017, the TCFD released its final report on climate-related financial disclosure recommendations designed to help companies provide credible information to support informed capital allocation.

How does TCFD work?

The TCFD recommendations guide all market players in terms of disclosing information about the financial ramifications of climate-related risks and emerging opportunities so that they may be included into business and investment choices.

Over 1,600 enterprises and organisations in almost 80 countries and six continents — with a combined market value of nearly $16 trillion – support or have already implemented the TCFD. Investors have begun to use it lately to evaluate the success of their own holdings.

The G7 nations (Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States) have made TCFD-aligned reporting obligatory.

%2520(1).avif)

What makes TCFD unique?

As it encourages companies to investigate further, the TCFD is distinct from other frameworks in that it can be used to structure an organisation's risk management systems.

By encouraging businesses to examine their operations, this reveals how they perceive sustainability from both governance and risk perspectives.

It can be used to inform an entire sustainability initiative through the deliberation of these variables. The latest public consultation conducted by the TCFD on transition plans and portfolio alignment expanded its scope to encompass the net-zero plan, which targets climate change's core causes rather than merely its consequences.

{{encartSpecial}}

Themes covered by TCFD

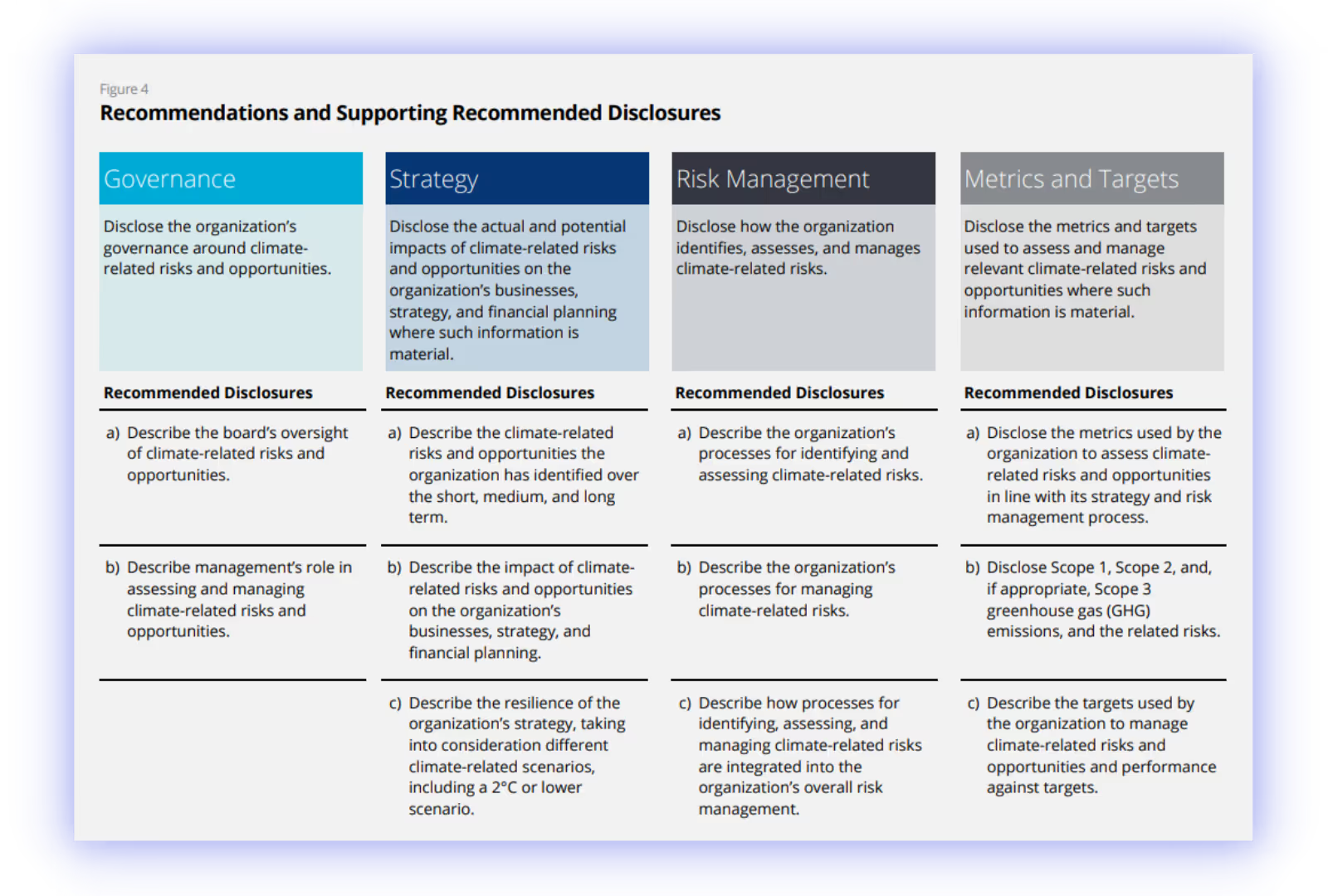

The signatories to the TCFD pledge to disclose their activity in four key areas, including the following:

- Governance - the way businesses manage the risks and possibilities associated with climate change

- Strategy - investigating the real and possible consequences of climate change on the company, strategy, and financial planning where such information is material

- Risk Management - defining the process through which an organisation identifies, evaluates, and manages climate-related hazards

- Metrics & Targets - metrics and targets used to assess and manage relevant climate-related risks and opportunities where such information is material

Additionally, the TCFD distinguishes between two categories of climate threats:

Physical risks

Physical risks stem from the consequences that most people associate with climate change and may be further categorised into two categories: acute and chronic. Acute physical threats are event-driven, and include a rise in the intensity of severe weather events like cyclones, storms, and flooding. Chronic physical threats develop due to longer-term changes in climate patterns, such as prolonged higher temperatures, which may result in rising sea levels or heat waves.

Transition risks

Transition risks develop because of the low-carbon economy's transition. They include regulatory and legal risks related to evolving technology and altering demand and consumption patterns, and reputational risks linked with an inability to appropriately adapt to climate change.

The four thematic areas of TCFD and their practical implications

As part of the TCFD recommendations, companies are advised to implement or highlight select elements in terms of governance, strategy, risk management, and measurements and goals.

Governance

- Highlight the board's supervision of risks and opportunities associated with climate change

- Describe the role of management in analysing and managing climate-related risks and opportunities

Strategy

- Define the climate-related risks and opportunities that the organisation has identified over the short, medium, and long term state the effect of climate-related risks and opportunities on the organisation's businesses, strategy, and financial planning

- Explain the resilience of the organisation's strategy in light of several climate-related scenarios, including a 2°C or lower scenario

Risk management

- Outline the methodology used by the organisation for identifying and analysing climate-related hazards

- Identify the methods that the organisation uses to manage climate-related risks

- Incorporate the methods for detecting, analysing, and managing climate-related risks into the broader risk management process of the organisation

Measurements and goals

- Reveal the indicators that the organisation uses to analyse climate-related risks and opportunities per its strategy and risk management approach

- Report greenhouse gas (GHG) emissions from Scope 1, Scope 2, and, if applicable, Scope 3 sources, and also the risks associated with these emissions

- Define the objectives that the organisation uses to manage climate-related risks and opportunities, as well as the organisation's performance concerning those targets

These four thematic areas are complemented by the following:

- 11 Supporting Disclosures - three supporting disclosures are recommended for each of the thematic categories, with the exception of governance, which contains two supporting disclosures; and

- Guidance for all Industries - the recommendations and accompanying disclosures are applicable to all industries. Supplemental advice goes into further detail about how certain industries in the financial and non-financial sectors are required to react to the suggestions made in the previous guidance. Industry-specific guidelines are aimed at the financial sector as well as 12 other sectors that account for the biggest amount of GHG, energy consumption, and water use, respectively.

- Supporting disclosures for certain non-financial and financial sectors — this guideline elaborates on how different industries can react to the required supporting disclosures;

- Illustrative metrics for non-financial sectors - the appendix contains further information on illustrative measures for non-financial industries.

How TCFD outlines financial impacts of climate-related risks and opportunities

According to the guidelines, climate risks and opportunities may have a financial effect on organisations' income statements and balance sheets.

As such, organisations are urged to consider providing the following under the category "income statement":

Potential positive and negative effects on their future revenues from changes in climate-related policies, technology, and market mechanisms, such as the possible effects of carbon pricing; and the magnitude to which their cost structure/expenditure is adequately adaptable to respond to the market cost and demand changes caused by climate risks and opportunities.

Organisations are encouraged to consider reporting the following information under the term "balance sheet":

- A proof of their assets and liabilities' climate-related profiles, with a particular emphasis on long-lived resources and reserves, and an emphasis on current and dedicated future actions and processes mandating new investment, restructuring, write-downs, or impairment;

- How their capital allocation strategies relate to climate risks and opportunities, and whether those proposals are sufficiently flexible in responding to shifting risks and opportunities.

What are the advantages of TCFD?

A few of the possible advantages connected with putting the Task Force's recommendations into action are as follows:

- Boosting the confidence of investors and lenders that the company's climate-related risks are effectively evaluated and handled, allowing for simpler or better access to finance

- Satisfying current disclosure standards to disclose important information in financial reports in a more efficient and effective manner

- Greater knowledge and understanding of climate-related risks and opportunities across the organisation, leading to improved risk management and more informed strategic planning

- Addressing investors' need for climate-related information proactively within a framework that investors are increasingly requesting, which may eventually lead to a reduction in the amount of climate-related information requests received

How to leverage TCFD?

The TCFD framework is not concerned with the final act of disclosure, but with the elements and indicators to disclose.

Rather than burdening businesses with extra reporting requirements, the TCFD principles have been aligned with current disclosure frameworks and guide a more effective reporting process. Finally, this will assist businesses in reporting and investors, lenders, and insurance underwriters comprehend serious risks.

The TCFD recommends that corporations consider the influence of climate change on their company operations, strategies, and financial planning.

When it comes to climate strategy, it should be aligned with the larger business plan, and there should be a clear understanding of how it will match with the organisation's operating model in the short, medium, and long terms.

- Climate risk duties and responsibilities allocated within the governance framework should be supported by board-level and enterprise-wide training and competence development in climate risk management.

- Identify areas of emphasis for disclosure around the four basic pillars of TCFD reporting by conducting an audit to identify gaps in the information available.

- Recognise the physical and transition risks and possibilities associated with climate change that are relevant throughout the organisation, considering the exposure to various industries, locations, and regions.

- Climate-related key performance indicators (KPIs) and risk metrics should be established.

- KPIs and climate risk metrics should be defined and tracked appropriately via the internal reporting systems.

- Identifying and managing business risks should include a formalised and documented discussion on climate risk among all stakeholders. According to the board-approved risk appetite, these risks should be included in the current enterprise-wide risk management framework.

All organisations must begin working toward adopting these reforms far in advance of being entangled in the web of mandatory disclosures and reporting obligations.

Firms that wait to comply until the last minute will not only struggle to meet compliance requirements as a result of the complexity of the process, but they will also miss out on the emerging opportunities that are associated with being aware of the exposure to climate-related risks and being an active contributor to a more sustainable economy.

When dealing with concerns connected to climate change, assessing financial risk may be difficult because of the scope, unpredictability, and long-term nature of the challenges.

There may be ramifications across the whole organisation if these risks are not properly managed.

Shifting client expectations and new regulatory requirements may influence revenues, whilst the availability and price of raw materials may have an impact on expenses. Investors and stakeholders require increasing transparency about how firms are analysing and responding to these risks.

Historically, the substantial focus has been placed on physical dangers, which, although more palpable than transition concerns, may arise over a longer time period. Nevertheless, transition risks may have a short-term effect on organisations: those that fail to appropriately identify them may expose themselves to severe commercial risk.

TCFD disclosure

Where should the information be disclosed?

The Task Force aspires to see climate-related information reported in mainstream reports (such as mainstream yearly financial statements) or other publicly available materials in the future.

If some aspects are incompatible with national disclosure laws, the Task Force recommends firms to publish such information in other official corporate reports, rather than in their annual reports.

In addition to using current channels of communication, asset owners and asset managers are urged to report to their beneficiaries and customers via publicly available channels of communication.

Preparing for TCFD disclosure

Assign responsibilities to colleagues in sustainability, governance, and compliance by getting them to meet and agree on them.

It is a primary objective of the Task Force to bring climate change problems up to the board level from the sustainability department of the company. However, this can only be achieved if your company implements integrated management practices.

There is an abundance of information on climate-related financial disclosures. Numerous reports, manuals, and other materials are aimed at assisting those who prepare disclosures.

TCFD Knowledge Hub

This website is powered by the Climate Disclosure Standards Board (CDSB), a division of CDP Worldwide.

As may be assumed, a substantial percentage of the Hub's content is directed towards those who write TCFD-related reports. Some of the things are industry-specific, while others are broader in scope. The resources cover various topics, including capital expenditures, investment requirements, carbon pricing, and scenarios.

The United Nations Environment Programme Finance Initiative (UNEP FI)

These guidelines have been convening 'TCFD Pilot Projects' with a number of member banks, investors, and insurers. These initiatives seek to pioneer practical framework implementation methods, and some have published reports summarising their experiences.

TCFD Good Practice Handbook

This guide offers firms' practical experiences with TCFD implementation and gives a variety of tools to assist companies in further improving their disclosure.

TCFD Implementation Guide

A practical "how-to" guide for firms wishing to put the TCFD recommendations into reality by using SASB standards and the CDSB Framework is provided in the TCFD Implementation Guide.

SASB and CDSB are two renowned organisations market employing TCFD-aligned reporting instruments, that support the implementation of the recommendation in conjunction with the 11 associated disclosures, in a cost-effective manner for both companies and investors

A framework for environmental, social, and governance (ESG) advice, the Sustainability Accounting Guidelines Board (SASB) establishes standards for the disclosure of financially important sustainability information by corporations to their shareholders.

The Climate Disclosure Standards Board (CDSB) is a non-profit organisation dedicated to providing meaningful information to investors and financial markets via the incorporation of climate change-related data into mainstream financial reporting practices.

Options for facilitation and aid from third-parties

With Apiday, it’s easier than ever to align your reporting with any framework! Including TCFD.

Our AI-driven technology gathers all your sustainability data in one place and automates the reporting process: on the Apiday platform, you’ll find a list of documents to share. Upload as many as you can find, and we’ll pre-fill your report wherever possible and provide you with a correspondence table.

While our experts assist you along the way with tailored ESG consulting support!

Save yourself time and hassle, and let Apiday do the rest!

Navigate the Complexities of TCFD with Confidence!

Our AI-powered tool simplifies your sustainability data collection process and generates comprehensive reports on your performance. You can gain the trust and engagement of stakeholders, attract responsible investors, and contribute to a more sustainable future. Let us help you take your reporting to the next level!

Frequently Asked Question

The Financial Stability Board (FSB) established the Task Force on Climate-Related Financial Disclosures (TCFD) in 2015 to provide uniform climate-related financial risk disclosures for corporations, banks, and investors when communicating with stakeholders.

The Task Force on Climate-related Financial Disclosures aims to see information about the financial impacts of climate change disclosed in mainstream reports or other publicly available materials. It is distinct from other frameworks in that it can be used to structure an organisation's risk management systems. The GRI Standards framework, on the other hand, is meant to help companies know what kind of ESG information they should disclose.

TCFD four pillars are: governance, strategy, risk management, and measurements and goals.

Sources

Related articles

What is the Sustainability Accounting Standards Board (SASB) and how does it work?

The SASB Standards cover a range of environmental, social, and governance (ESG) topics, and are designed to be compatible with existing financial reporting frameworks.

What is the ESG reporting standards landscape?

Explore the ESG reporting standard landscape and find the right fit for your organisation.

What is the ESG reporting regulations landscape?

Explore the ESG reporting standard landscape and find the right fit for your organisation.